03 February 2026

5 min read

By Lara Sinclair

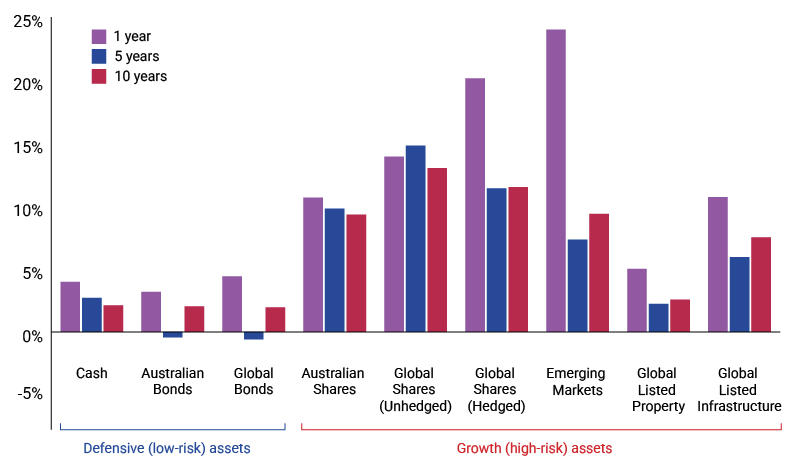

Emerging markets, led by China, were the top-performing investment type, with a net return of 24.0% for the 12 months to 31 December 2025.

Summary

Emerging markets, led by a reassessment of many under-valued Chinese companies, delivered returns that were 2.5 times their 10-year average last year.

Sharemarkets again dominated the headlines in 2025, but investors seeking strong returns had a much broader range of investment types from which to choose than in recent years, which were dominated largely by US technology share price surges.

The strongest returns by investment type for the 12 months to 31 December 2025 came from emerging markets, which returned an impressive 24.0%, and hedged global shares, which offered returns of 20.1%1.

In a year marked by chaotic policy announcements from the US government – most notably the introduction of ‘Liberation Day’ tariffs on 2 April – investors looked to diversify their investments to protect the value of their money.

The demand for gold continued to climb, reaching record heights2, while the US dollar – traditionally seen as a ‘safe haven’ in times of uncertainty – weakened by about 9% against six other major currencies3 over the course of the year.

Australian shares – particularly smaller companies buoyed by gold exposure, global listed infrastructure and bonds also offered solid gains compared with their 10-year average1 while cash returned 4.0%, almost double its 10-year benchmark of 2.1%.

How major investment types performed over 1, 5 and 10 years

CFS Research and Performance data. Annualised performance for periods over 12 months to 31 December 2025. Benchmark performance is shown for key indices.1

Emerging markets lead the way

Emerging markets – encompassing stocks traded in less mature markets than the US, Europe and Japan (EM) – delivered performance last year that was 2.5 times higher than their 10-year average return of 9.4%.

CFS Chief Investment Officer Jonathan Armitage says the CFS Investment team increased its allocation to these markets – which are dominated by China, Taiwan, India and South Korea – early in response to a significant gap between how western companies and those in emerging markets were being valued.

Earnings streams were being undervalued, and the launch of Chinese AI product DeepSeek sparked a “general re-think” among global investors. “The strength of China in particular but also Asian markets as a whole probably caught people off guard,” Jonathan says.

As part of its re-allocation, CFS consolidated some of the fund managers it was using and employed a mix of active analysis and systematic strategies – based on identifying patterns in market data – to identify undervalued stocks.

“Emerging markets used to be all about growth, but now value is a very strong driver of returns,” Jonathan says.

Meanwhile, a trip to China late last year reinforced the view that companies in China are now developing service capabilities that move them up the value chain and increase their profitability. Combined with their ability to compete with western companies on price, this makes them a “significant threat” to western business models.

While China was the top-performing market, the AI hardware trio of Taiwan Semiconductor Manufacturing Company and South Korean companies Samsung and SK Hynix, helped generate strong returns. Gold‑linked sectors also performed well, helped by the high price of gold bullion.

Hedged global shares outshine unhedged

Tech stocks remained influential throughout 2025, though strong earnings were no longer enough to drive the explosive share price growth of recent years.

Still, Jonathan believes it’s too early to say that the US has lost its appeal: “It’s still the world’s largest, deepest, most sophisticated capital market.”

Global share investors had reason to celebrate, with hedged global equities returning 20.1% -- well above their 10-year average return of 11.5%.

Hedged portfolios remove the influence of currency fluctuations, so a strengthening Australian dollar did not affect investment returns at the end of 2025.

Unhedged global shares slipped into negative territory in December but stayed above their 10-year average 13.0% return.

CFS took out a long‑dated insurance policy on the US market when valuations made it seem prudent, part of its dynamic asset allocation approach to risk.

Despite that, Jonathan says there is too much focus on whether an AI-driven market bubble is developing and warned against pulling money out of the US market. “We continue to find a broad breadth of opportunities in the US, both in liquid and unlisted markets,” he says.

Smaller Australian companies outperform bigger rivals

Closer to home, Australian shares rose 10.7%, 1.4% above their 10-year average return.

However, the real growth came from smaller Australian companies, or “small caps”, which delivered returns of about 25% for the year.

Their 27% weighting to the materials sector, particularly gold miners, provided a powerful boost as gold prices hovered at record highs.

Bonds perform well in 2025 as pressure builds

Bonds offered strong performance over the 2025 calendar year: global bonds delivered above-average returns of 4.4% and Australian bonds 3.2% last year.

However, high government deficits in the US and Europe continue to provoke questions from investors, and Jonathan says these pressures are likely to persist.

Concerns about continuing government spending and unpredictable US government actions – resulting in some central banks reconsidering their exposure to US Treasury bonds – also affected bond markets in 2025.

Global listed infrastructure posts strong returns

Global listed infrastructure returned 10.7%, well above its 7.5% average over 10 years, benefiting from continued spending on the transition to renewable energy, and digital connectivity.

Global listed property performed slightly above its 10-year benchmark, delivering a 5.0% return.

Inflationary pressures likely to keep a lid on returns

After three strong years of investment performance, Jonathan says more modest results are likely, with fiscal concerns and inflation pressures likely to act as a ‘cap’ on returns.

In 2026, CFS remains focused on diversification, valuation discipline and dynamic risk management and we expect returns to come from a wider range of investments over the coming year.

Looking to invest?

CFS offers more than 200 investment options, so there's something to suit everyone.

Related articles

Too late to go for gold in 2026?

With gold prices continuing to break records this year, we examine the outlook for this ‘safe haven’ investment.

Top performing investment options of 2025

Which investment options delivered the best performance, ranked by their returns over 12 months?

Star investment types of 2024-25

The best performers for investors seeking high returns broadened to new sectors.

1 Source: Colonial First State Research and Performance data. Annualised performance for periods over 12 months to 31 December 2025. Benchmark performance is shown for: Bloomberg AusBond Bank Bill Index; Bloomberg AusBond Composite 0+ Yr Index; Bloomberg Global Aggregate AUD Hedged; S&P/ASX 300 Accumulation Index; MSCI ACWI Ex-Aus Index Special Tax Net AUD Unhedged; MSCI ACWI Ex-Aus Index Special Tax Net AUD Hedged, MSCI Emerging Markets (AUD), FTSE EPRA/NAREIT Dev ex Aus Rental Index AUD Hdg Net and FTSE Dev Core Infrastructure Index AUD Hdg Net.

2 Source: Bloomberg, XAU:CUR gold spot price, 12 months to 31 December 2025.

3 Source: Bloomberg, US dollar index, 12 months to 31 December 2025.

Disclaimer

Avanteos Investments Limited ABN 20 096 259 979, AFSL 245531 (AIL) is the trustee of the Colonial First State FirstChoice Superannuation Trust ABN 26 458 298 557 and issuer of FirstChoice range of super and pension products. Colonial First State Investments Limited ABN 98 002 348 352, AFSL 232468 (CFSIL) is the responsible entity and issuer of products made available under FirstChoice Investments and FirstChoice Wholesale Investments.

Information on this webpage is provided by AIL and CFSIL. It may include general advice but does not consider your individual objectives, financial situation, needs or tax circumstances. You can find the target market determinations (TMD) for our financial products at https://www.cfs.com.au/tmd which include a description of who a financial product might suit. You should read the relevant Product Disclosure Statement (PDS) and Financial Services Guide (FSG) carefully, assess whether the information is appropriate for you, and consider talking to a financial adviser before making an investment decision. You can get the PDS and FSG at www.cfs.com.au or by calling us on 13 13 36.