26 February 2026

4 min read

By Sergio Magliarachi

Want to set up an SMSF? Understand how it works - and whether it's right for you - before you take the wheel.

Summary

A self-managed super fund (SMSF) may give you more control and choice, but it also comes with extra paperwork, many rules, and may be tricky to start. Here’s a simple step‑by‑step guide to setting one up, what it can cost, and the pros and cons to weigh up before you decide if an SMSF is right for you.

Like podcasts? You'll love this article, now in audio.

Skip the scroll and listen to the audio summary at home, on the go, or wherever you are.

In this short episode, we’re talking about self-managed super funds – or SMSFs – and what you need to know before you think about setting one up. A simple way to picture an SMSF is like a four‑wheel drive. In the right conditions, it may take you further and give you more control. But it also needs more upkeep, more attention and a bit more know‑how than a regular run‑around car – in this case, a regular super fund.

So what’s the appeal?

An SMSF may give you more investment choice, including things like direct property and other specialist investments. You get more flexibility in how the fund is run, and more control over decisions – including which tax, legal and financial professionals you work with and what strategy to follow. You’ll need to decide on a structure, and appoint trustees to manage the fund.

For people with higher balances, SMSFs may sometimes be more cost‑effective because many of the costs are fixed. And you may have more ways to manage tax outcomes within the super rules.

But that extra control comes with trade‑offs.

There’s more admin and paperwork, and you need to stay on top of changing rules. There are legal responsibilities for trustees, and if these responsibilities are not followed, significant penalties may apply. Fixed costs may make SMSFs less cost‑effective for smaller balances, and life events – like divorce, death or someone moving overseas – may make running the SMSF more complicated.

You’ll also may have fewer safety nets than some other financial products if something goes wrong.

If you do go ahead, there are a few big building blocks:

choosing your trustee structure, putting a solid trust deed in place, making sure assets are held in the right name, registering the fund with the ATO, setting up a dedicated bank account and electronic service address, and putting a written investment strategy and exit plan in place.

In our case study, Daniel and Priya – in their late 40s with a combined balance of $950,000 – tick through this checklist step by step. They choose a corporate trustee, get a tailored deed, set up the right bank account and service address, agree on their investment strategy and, importantly, outline an exit plan. Then they keep a simple yearly routine to stay on top of the fund's investments, audits and reporting – so it’s steady admin, not a last‑minute scramble.

The big message? An SMSF may give you more control – but it’s not for everyone.

Getting professional advice (such as tax, legal and finanical) may help you decide if an SMSF is right for you, choose the right structure and set it up correctly from day one. At Colonial First State, there are different advice options available, including some at no additional cost, to help you get clear on your next step.

Setting up a self-managed super fund (SMSF)

A handy way to think about SMSFs is like a four-wheel drive: a special-purpose vehicle built for people with specific needs and the confidence to handle the extra features. It offers control and flexibility, but it may also mean more responsibility, more upkeep, and more know‑how. So if your needs are simple, a regular super fund may already have the features for your needs.

While SMSFs may give you more choice and flexibility, this may also means more responsibility. SMSFs are tightly regulated. Meaning you'll be required to comply with some complex super and tax rules and do regular reporting from day one.

Please consider getting financial advice before making an investment decision.

An SMSF has a few key moving parts that all need to work together. They all sit inside a framework of super rules and tax rules, overseen by the ATO as the regulator. ASIC also play a role in regulating the gatekeepers – the accountants, financial planners, auditors and product providers.

In practice, that means making sure you have the right elements in place, such as:

- The right trustee structure - all members need to act as individual trustees, or as director of a company acting as trustee

- A properly prepared trust deed - the SMSF's own rulebook

- A documented investment strategy that considers the need to hold life insurance

- The right legal ownership of the fund's assets

- Importantly, the ability to meet the ongoing admin obligations. This includes keeping records, preparing fund reporting, arranging an annual audit, preparing the SMSF’s annual tax and compliance return, and then lodging it.

An SMSF has multiple parts - trustee structure, trust deed, investment strategy, assets and admin. All of it must comply with super and tax laws, and with the ATO as the regulator.

Pros and cons of self-managed super funds

Here’s a simple, broad look at the possible advantages and disadvantages of running your own super fund.

Pros

- Investment choice

SMSFs may offer more choice than many large funds, including things like direct property and cryptocurrency. - Flexibility

You can implement your own tailored investment strategy and decide what types of investments the fund invests in. - Control

You get to decide which professionals you work with, such as tax, legal and financial experts. You also have control over when and how benefits are paid. - May be more cost-effective for higher balances

Because many SMSF costs are fixed, the SMSF structure may suit some people with larger balances. - More options to manage tax outcomes

Super has its own tax rules and obligations. With an SMSF, you may have more control over timing and strategy; however, the rules may be complex, and seeking tax, legal and financial advice is recommended.

Cons

- More paperwork

There’s significant admin, record-keeping, reporting, and compliance work every year. - More time and effort

You need to stay involved and keep up with laws, rules, and obligations to ensure compliance. - You may need to live in Australia

Residency rules generally mean you must physically be in Australia. So, you need to consider your individual circumstances if you spend long periods overseas. - More duty and responsibility

Trustees have legal obligations. If these rules are broken, penalties may apply to individuals and the fund. - Costs may be high for smaller balances

Fixed costs may make SMSFs less cost-effective when comparing small and large funds. - Harder and more expensive to unwind

Closing an SMSF may be complex, especially if the assets are hard to sell. Selling assets within an SMSF often requires agreement from all trustees. - Changes in members’ lives may create problems

Things like death, divorce, bankruptcy, or someone moving overseas may have a big impact on how an SMSF is taxed and how it works. - Fewer safety nets

If you manage your own SMSF, it’s important to know you may not have the same protections applicable to members of larger super funds. This includes safeguards in cases of theft or fraud, and access to low‑cost dispute resolution services.

How much does it cost to set up an SMSF?

SMSF costs fall into two main buckets: set‑up costs and ongoing yearly costs.

Set-up costs

These may include:

- Legal documents to create the SMSF.

- Legal and financial advice to transfer benefits to an SMSF.

- Setting up a corporate trustee, if you choose that structure.

- Using an accountant or SMSF admin provider to set up and manage ATO registration.

Ongoing yearly costs

These may include:

- Administration.

- Accounting and tax reporting.

- An independent annual audit.

- Ongoing legal and financial advice.

The key thing to remember is that many SMSF costs are fixed. That’s why SMSFs may be relatively expensive for smaller balances, and why people often compare SMSF costs differently to large super funds.

How long does it take to set up an SMSF?

Some SMSFs may be set up within a few weeks, but timing depends on factors like:

- How quickly paperwork is prepared and signed.

- Whether you choose a corporate trustee.

- The registration process.

- Setting up the required bank accounts and electronic service providers.

- How long rollovers from existing super funds take.

- Whether you’re setting up borrowing arrangements.

Step-by-step guide to setting up an SMSF

Here’s the typical setup process.

1. Choose your trustee structure

SMSFs usually use one of two setups:

- Individual trustees: the members are the trustees.

- Corporate trustee: a company is the trustee, and members are directors of that company. A dedicated trustee company may help keep SMSF duties separate and simpler.

A corporate trustee may cost more upfront, but some people may find it simpler in the long-term . Especially if there are later changes to members.

2. Appoint your trustees

There are different requirements based on your trustee structure.

For individual trustees, each member of the fund will need to be appointed as a trustee, and all trustees will need to be a member of that fund.

For corporate trustee structures, each member of the fund will need to be appointed as a director, and all directors will need to be a member of that fund.

3. Create the SMSF trust deed

The trust deed contains the rules for the SMSF. It explains what trustees can and can’t do. It’s the key document relieiedd on if a dispute arises.

4. Appoint admin service provider

An SMSF admin service provider helps to set up and run the fund.

5. Set up how the SMSF will hold assets

SMSF assets need to be held in the correct name.

6. Sign the trustee declaration

This step requires Trustees to sign a declaration confirming their obligations, and the fund must be registered and regulated by the ATO.

7. Set up a bank account

Your SMSF needs its own bank account to receive contributions and rollovers, pay bills, and manage investments.

8. Get an electronic service address

This helps the SMSF receive contributions and rollovers electronically through the same SuperStream system used by super funds and employers.

9. Create your investment strategy

An SMSF must have an investment strategy which is a written plan that guides how the fund invests. This should include:

- Your retirement goals and timeframes.

- Investment choice.

- Liquidity, or having cash available to pay costs and benefits.

- Risk profile.

- Whether to hold life insurances for members.

10. Prepare an exit plan

Not many people think about this at the start, but it’s important. An exit plan helps you think through scenarios such as:

- When you might close the SMSF in the future, for example due to advancing age or declining health.

- What happens if members’ circumstances change or if they leave the SMSF.

- How you’d sell or transfer assets.

Case study: Daniel and Priya set up an SMSF to take more control of their super

Daniel and Priya are in their late 40s with $950,000 in combined super.

They want more control and a clean, compliant SMSF set‑up, so they follow a clear checklist and make key decisions early.

1) Trustee structure:

They set up a company to act as trustee - a corporate trustee - and make themselves the directors. This is the most common structure across SMSFs, and it allows for later changes to members.

2) Appoint directors:

They both become directors of the trustee company, so the structure meets the SMSF rules. They agree they'll be involved in running the fund and in making all the key strategic decisions.

3) SMSF trust deed:

They set up a trust deed that names trustees and defines the SMSF rules.

4) Appoint an admin service provider:

They appoint service providers, such as an SMSF admin service provider, to help them set up and run the fund.

5) Sign declaration:

They sign the SMSF trustee declaration and fill out the required paperwork to register the SMSF, allowing it to be regulated by the ATO.

6) Bank account:

They open a dedicated SMSF bank account and use it for everything. This includes rollovers, contributions, investment income, and expenses.

7) Electronic service address:

They get an electronic service address so contributions and rollovers can be received electronically.

8) Investment strategy:

Before investing, they write their investment strategy that aligns to their goals, risk comfort, diversification needs and the fund’s ability to meet fees.

9) Exit plan:

They put an exit plan in writing early so they’ve already agreed what they’ll do if they ever want to close the fund. This helps reduce the risk of potentially expensive, last‑minute decisions later on.

How they keep compliance on track long-term:

Daniel and Priya set a recurring yearly routine: They take time to review their investment strategy, confirm their assets still align with it, and keep the right records on hand.

They also book in their annual audit and prepare what’s needed for their annual reporting and return. That way the SMSF’s admin becomes a steady, manageable task rather than a once‑a‑year scramble.

Getting financial advice for property investing through super

It takes time and careful decision-making to set up your SMSF the right way.

Getting professional advice, such as tax, legal and financial, may help you:

- Decide if an SMSF is right for you.

- Choose the right structure.

- Set it up correctly from the start.

- Build an investment strategy that fits your goals.

- Understand your responsibilities and ongoing obligations.

- Ensure compliance with laws, rules and obligations.

That’s why Colonial First State offers financial advice options. They range from comprehensive, ongoing advice with a financial adviser who specialises in SMSFs, to more general advice which may point you in the right direction.

Is an SMSF the right option for you?

Starting an SMSF isn’t for everyone. It requires careful consideration, commitment, and some financial expertise. Find out if it's the right move for you, and how we can help support your goals.

Related articles

CFS Market Insights: What's shaping the outlook for 2026

Strong returns held up in 2025 as new growth opportunities emerge across global markets in 2026.

Is your super investment mix right for you?

How do you know if your super investment mix is right for you? The right option could result in tens of thousands of dollars more in your super.

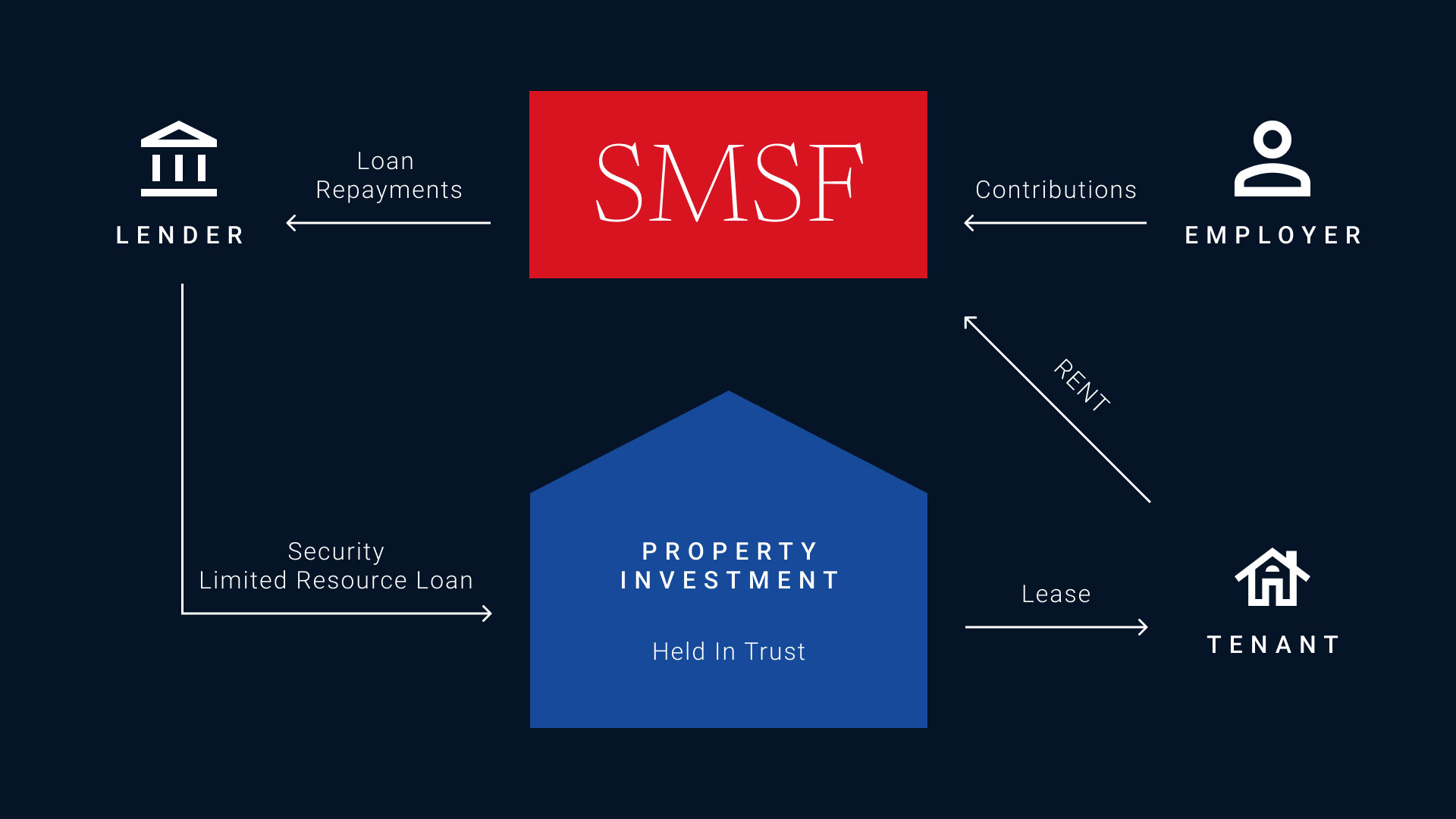

Property and SMSFs: Buying property with super

Learn everything you need to know about property investing through a SMSF, including important rules, whether it might be the right move for you, and how to get started.

Disclaimer

Avanteos Investments Limited ABN 20 096 259 979, AFSL 245531 (AIL) is the trustee of the Colonial First State FirstChoice Superannuation Trust ABN 26 458 298 557 and issuer of FirstChoice range of super and pension products. Colonial First State Investments Limited ABN 98 002 348 352, AFSL 232468 (CFSIL) is the responsible entity and issuer of products made available under FirstChoice Investments and FirstChoice Wholesale Investments.

Information on this webpage is provided by AIL and CFSIL. It may include general advice but does not consider your individual objectives, financial situation, needs or tax circumstances. You can find the target market determinations (TMD) for our financial products at https://www.cfs.com.au/tmd which include a description of who a financial product might suit. You should read the relevant Product Disclosure Statement (PDS) and Financial Services Guide (FSG) carefully, assess whether the information is appropriate for you, and consider talking to a financial adviser before making an investment decision. You can get the PDS and FSG at www.cfs.com.au or by calling us on 13 13 36.