Coming in the second half of 2026

Deliver more certainty, flexibility and confidence in retirement

The Retirement Income Optimiser is a built‑in feature of FirstChoice super that allows you to support lifetime income strategies, without locking your clients into decisions while they are still building their super.

In combination with a CFS lifetime pension option (currently in development, and expected to be launched in 2027), it enables you to structure income at retirement in a way that may improve Age Pension outcomes and overall retirement income for your clients.

By bringing lifetime income and potential Age Pension benefits together it can help your clients receive a higher overall retirement income.

A complementary retirement income strategy

The Retirement Income Optimiser works alongside your clients’ super and, when used in combination with a CFS lifetime pension at retirement, can help manage how your clients’ assets are assessed for Age Pension purposes later in life.

In addition, it allows you to:

- introduce an income stream for life for your clients

- depending on what is appropriate for the client, retain growth and liquidity through an account-based pension

- manage sequencing risk and longevity risk together

- tailor outcomes to each of your client’s personal and Centrelink circumstances.

You retain the flexibility to design a retirement income strategy for your clients that aligns with their goals, timeline and confidence level.

The Retirement Income Optimiser in super

Once switched on, the Retirement Income Optimiser operates automatically within a client’s FirstChoice Wholesale Personal Super account unless they opt out. There's no additional cost to keep the feature active.

While your client is still in super:

- their account operates exactly as normal

- investment options, fees, insurance (if applicable) and contribution strategies are unchanged

- no retirement income decisions are required

- no capital is set aside or locked away

The feature simply preserves a future lifetime income option, giving you greater strategic flexibility at your client’s retirement.

The Retirement Income Optimiser at retirement

When a client meets a condition of release, they have the option of commencing a CFS lifetime pension (when the product is available) which will pay an income for life and can be commenced immediately, or deferred to a later date.

Clients can choose how much of their super balance to allocate to a lifetime pension. When they meet a condition of release they need to tell us within 14 days what they would like to do.

If they choose to allocate part of their super to a lifetime pension, the Retirement Income Optimiser helps determine the Purchase Amount that Centrelink uses under the Age Pension assets test for the lifetime pension. It calculates this amount separately from the client’s actual super balance. In broad terms, the Purchase Amount:

- reflects the client’s initial balance and net contributions over time

- sees each amount indexed annually using the Centrelink upper deeming rate (currently 3.25%) until they meet a condition of release. No further indexation applies after they meet a condition of release.

- is reduced by commutations, including to purchase an account-based pension

- when calculating the assessable asset value of a lifetime pension, 60% of the Purchase Amount is assessable until age 85, then it reduces to 30%

Because Centrelink may assess this Purchase Amount rather than the full value invested in the lifetime pension, this structure may improve your client’s Age Pension eligibility, depending on their individual circumstances and government rules at the time.

Why starting early can matter for your clients

Because the deemed Purchase Amount may be less than the full account balance invested in the lifetime pension, this may result in a lower assessable asset value than the actual account balance used to purchase a lifetime pension.

The longer the client has the Retirement Income Optimiser feature applied, the greater the difference between the Purchase Amount and the actual account balance may be (assuming investment earnings exceed the upper deeming rate).

This means:

- clients may receive a higher Age Pension entitlement if they choose to allocate part of their super to an eligible lifetime income stream, depending on their circumstances

- no change to how your clients currently save or invest their super

- no commitment to a lifetime pension required until meeting a condition of release

- no impact on their overall super balance

Instead, the Retirement Income Optimiser can provide greater strategic opportunities for your clients’ individual retirement planning later in life.

See how Retirement Income Optimiser could affect Age Pension outcomes at retirement

Harry is 47 and has $200,000 in a FirstChoice Wholesale Personal Super account. His employer makes super guarantee contributions based on a salary of $100,000 p.a.

The built-in Retirement Income Optimiser feature is working in the background until he retires. At age 65 he meets a condition of release and advises his super fund that he would like to delay commencing a lifetime pension until he retires at age 67.

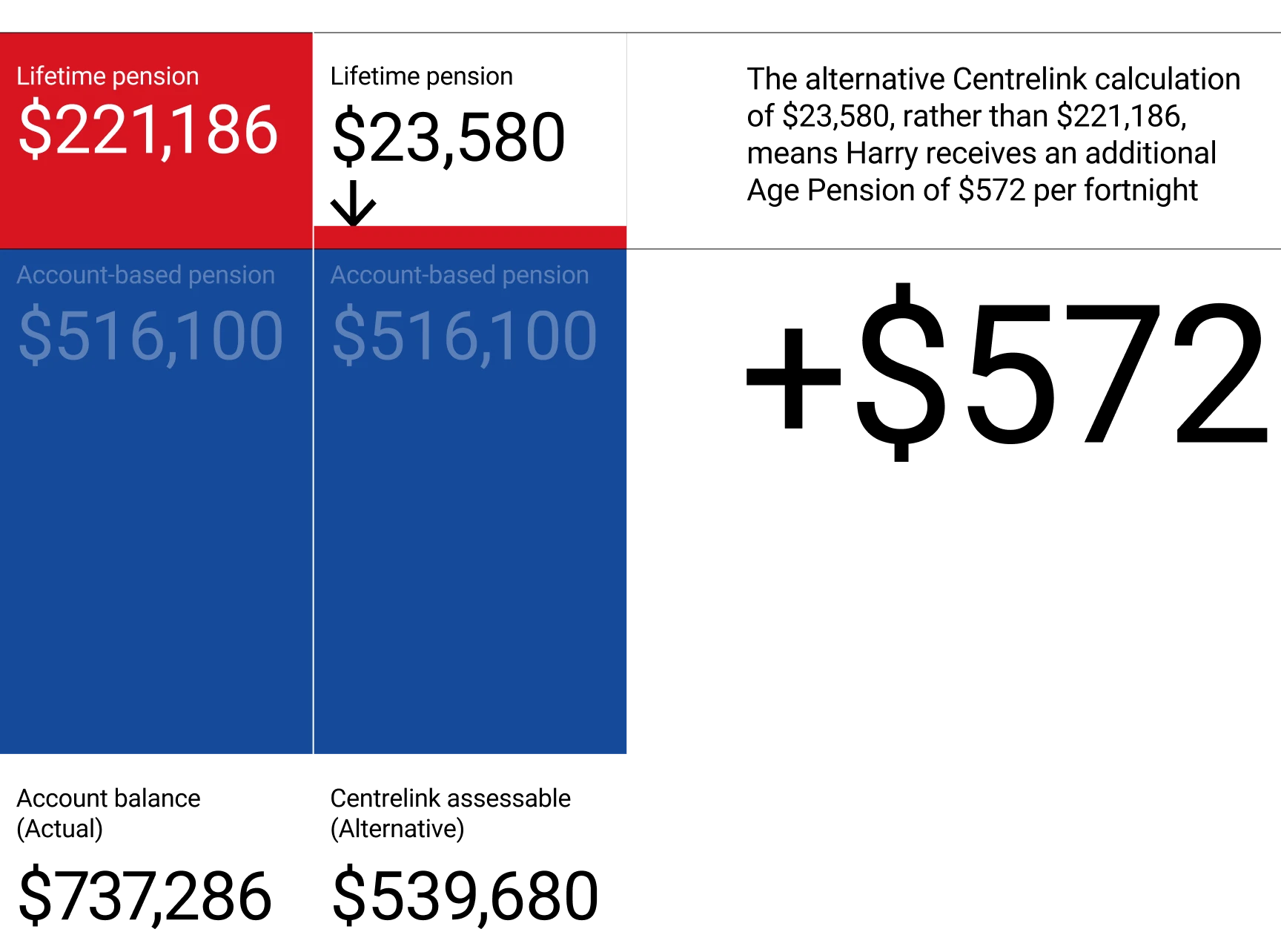

Harry's Super at 67

At retirement, Harry’s super balance has grown to $737,286.

He decides to purchase an account-based pension with 70% of his super balance and he allocates the remaining 30% to the lifetime pension.

Due to the Retirement Income Optimiser feature, when Centrelink calculate the assessable asset value of the lifetime pension, only $23,580 gets assessed. This results in Harry receiving an additional $572 per fortnight in Age Pension.

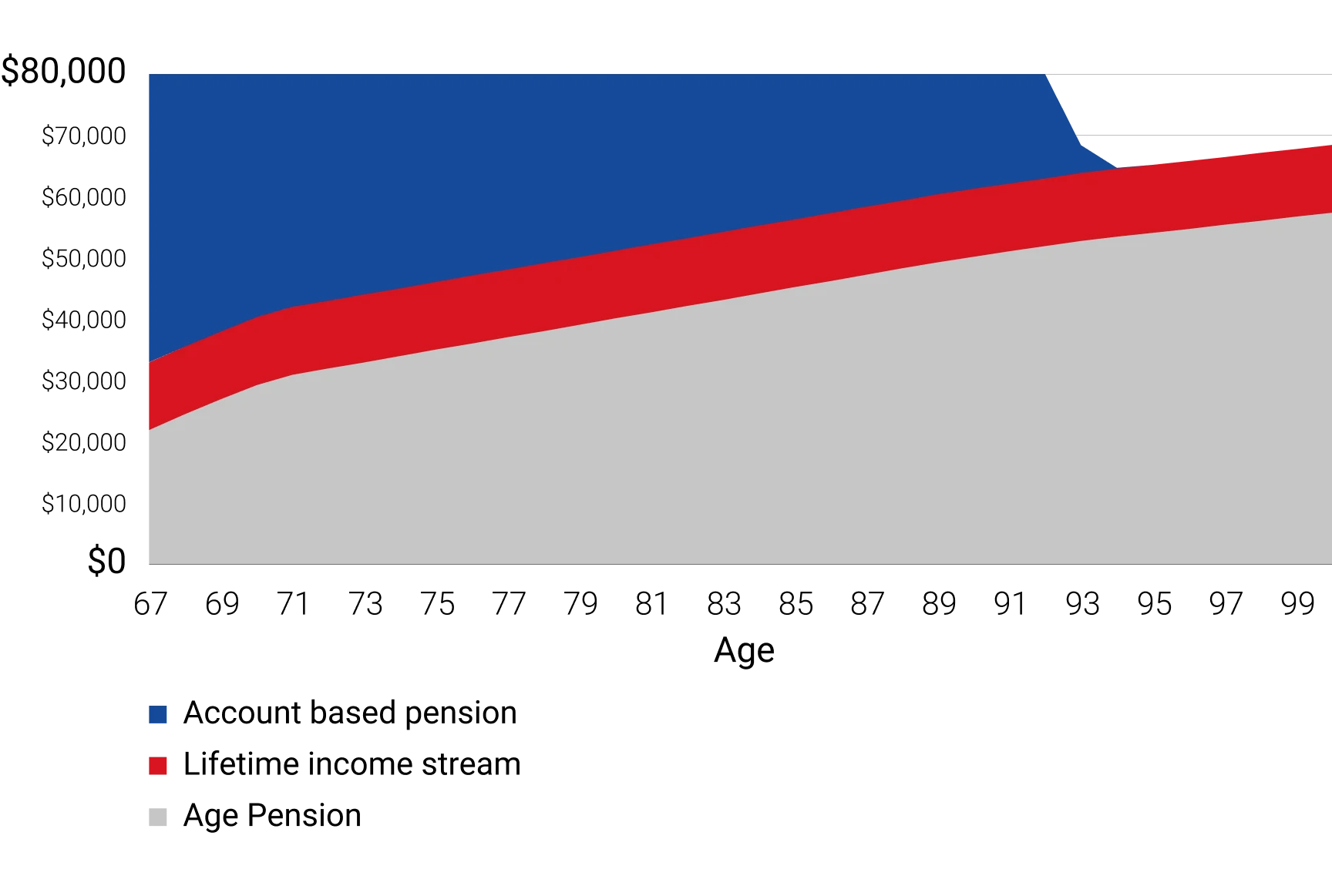

Harry’s retirement income projection

Harry’s income in retirement is a mix of income from his account-based pension, lifetime pension and the Age Pension, with the lifetime pension and Age Pension providing an income for life.

This example uses a number of assumptions and may not reflect the actual outcomes of any particular person. It is based on our understanding of relevant laws and regulations as at May 2026 and is subject to change. The information is of a general nature only. It is not intended to constitute financial, taxation or legal advice and should not be relied on as such.

- All results in today’s dollars (assuming CPI 2.5% p.a.).

- Lifetime pension: 5% per annum annual payment indexed to CPI of 2.5%. As the lifetime pension product is not yet available in FirstChoice, this lifetime pension projection is for illustrative purposes only and does not represent the product features or recommendation on the annual payment rate.

- SG 12% on salary of $100,000 indexed at 3.7%

- Earning rate 6.2% (net of tax and fees) from age 47 to 65, and 6.7% p.a. (net of fees) from age 65 in accumulation super and account-based pension

- Assumed upper deeming rate 5% p.a. At age 67, deemed purchase amount $555,400 less account-based pension commutation $516,100 = $39,300. Centrelink assessable asset value = 60% x $39,300 = $23,580.

- Age pension calculation assumes $10,000 other assets and single homeowner

- Additional Age Pension of $572 per fortnight at age 67 compares Age Pension if superannuation 100% assessable in an account-based pension, compared to Age Pension if 30% invested in lifetime pension using the Retirement Income Optimiser feature and 70% in an account-based pension.

- Retirement income projection assumes Harry requires $80,000 p.a. (today’s dollar) in retirement from a combination of Age Pension, lifetime pension and Age Pension.

- This image is for illustrative purposes only and does not constitute advice.

Important things to know

- Withdrawals, rollovers or transfers may reduce any potential Age Pension benefits if the client has the Retirement Income Optimiser feature applied and later chooses to commence a lifetime pension.

- Clients can choose to opt out of the Retirement Income Optimiser feature. However, if they do, this means Centrelink will not use the deemed Purchase Amount calculation when calculating the assessable asset value of a lifetime pension. This may result in a reduced Age Pension compared to having the feature apply.

- Lifetime pensions that comply with a capital access schedule receive concessional Centrelink treatment. The capital access schedule limits the amount that a client can receive if they die or voluntarily commute their lifetime pension. No death benefit or voluntary commutation amounts are payable once the client reaches their life expectancy.

- CFS doesn’t currently offer a lifetime pension. This product is still being developed. If a client meets a condition of release before a lifetime pension is available, the feature will be switched off without affecting their super account.

- Whether this feature is right for your client will depend on their personal circumstances.

- The above example uses a number of assumptions and may not reflect the actual outcomes of any particular person. It is based on our understanding of relevant laws and regulations as at May 2026 and is subject to change. The information is of a general nature only. It is not intended to constitute financial, taxation or legal advice and should not be relied on as such.

For more details, see the FirstChoice Super Product Disclosure Statement and Reference Guide.

Frequently asked questions

The Retirement Income Optimiser is a feature built into your clients’ super accounts that helps optimise their retirement outcomes by potentially increasing their future Age Pension entitlement. It works in the background of their super, without changing how they invest or manage their account.

The Retirement Income Optimiser is expected to be launched in the second half of 2026. Please check this page for the launch date.

The Retirement Income Optimiser takes into account IRIS (Innovative Retirement Income Stream) legislation, and is designed to convert to a lifetime income stream in retirement (either immediately or deferred to a later date), where elected by the client. The Retirement Income Optimiser helps determine the Purchase Amount that Centrelink uses under the Age Pension assets test for the lifetime pension. It calculates this amount separately from the client’s actual super balance.

It doesn’t change how your clients’ super works today, but it can help improve their options and potential Age Pension outcomes later.

The Retirement Income Optimiser allows eligible super balances to be treated differently for Age Pension calculations if your client chooses to commence a lifetime pension in retirement, either immediately or deferred to a later date.

This different treatment can increase the amount of Age Pension they may receive in retirement, depending on their circumstances.

Once the Retirement Income Optimiser is launched:

- FirstChoice Wholesale Personal Super clients don’t have to do anything. The Retirement Income Optimiser is automatically switched on for eligible members in FirstChoice Wholesale Personal Super. Your clients can choose to opt out at any time if it’s not right for them.

- FirstChoice Employer Super clients will need to actively choose to opt into this feature. By opting into the feature, it will change their account from ‘MySuper’ to ‘Choice’ but their fees, services, insurance and investment options stay the same. The option to opt into this feature will be available once it is launched.

You can send a Change of Details form signed by your client to CFS to switch the feature off.

The Retirement Income Optimiser feature will track your clients’ contributions and withdrawals over time to calculate what’s known as their Purchase Amount - the value used by Centrelink when assessing the value of a lifetime pension issued by us under the assets test.

Your clients’ Purchase Amount is calculated as the sum of their contributions (less any tax required to be deducted), compounded annually by the upper threshold deeming rate (currently 3.25% as at 20 March 2026), less any withdrawals (including rollover to another super fund, transfer to another FirstChoice account, transfer to a FirstChoice pre-retirement pension).

Withdrawals, rollovers or transfers may reduce any potential Age Pension benefit if your client later starts an eligible lifetime pension issued by us.

When calculating the assessable asset value of a lifetime pension, 60% of the Purchase Amount is assessable until age 85, then it reduces to 30%.

The deemed Purchase Amount calculation method may offer a more favourable means test assessment, potentially increasing your Age Pension entitlement. Age Pension outcomes depend on individual circumstances and the rules applying at the time.

The Retirement Income Optimiser allows eligible super balances to be treated differently for Age Pension calculations if they later move into an eligible lifetime pension. However, depending on individual circumstances, the alternative calculations may not change their social security outcome if they already qualify for the maximum Age Pension throughout retirement because of limited assets and income, or would not qualify for the Age Pension at all throughout retirement due to significant assets or income.

We're here to help

Get in touch

For adviser services contact us 8:30am - 6pm (Sydney time) Monday to Friday.

FirstTech: 9am - 5:30pm Monday to Friday.

Disclaimer

Avanteos Investments Limited ABN 20 096 259 979, AFSL 245531 (AIL) is the trustee of the Colonial First State FirstChoice Superannuation Trust ABN 26 458 298 557 and issuer of FirstChoice range of super and pension products. Colonial First State Investments Limited ABN 98 002 348 352, AFSL 232468 (CFSIL) is the responsible entity and issuer of products made available under FirstChoice Investments and FirstChoice Wholesale Investments.

Information on this webpage is provided by AIL and CFSIL. It may include general advice but does not consider your individual objectives, financial situation, needs or tax circumstances. You can find the target market determinations (TMD) for our financial products at https://www.cfs.com.au/tmd which include a description of who a financial product might suit. You should read the relevant Product Disclosure Statement (PDS) and Financial Services Guide (FSG) carefully, assess whether the information is appropriate for you, and consider talking to a financial adviser before making an investment decision. You can get the PDS and FSG at www.cfs.com.au or by calling us on 13 13 36.