Even a small difference in super fees can have a big impact on your retirement balance over time.

One of Australia's lowest administration fees

At Colonial First State, we believe your money should be working for your future, not eaten away by unnecessary costs. That's why CFS offers one of the lowest administration fees in Australia through CFS FirstChoice Wholesale Personal Super, so more of your super stays invested and has the chance to grow.¹

Every dollar saved on fees is a dollar that stays invested

Think of it this way: every dollar you pay in fees is a dollar that isn't growing through investment returns. And because super compounds over decades, that one dollar doesn't just disappear, it takes its future earnings with it.

This is why fees matter more than most people realise. A super fund that charges even half a per cent more in admin fees can cost you thousands over a working career, not because the fee itself is large, but because of what that money could have earned if it had stayed invested.

Lower fees don't guarantee better returns, but they do mean more of your money is in the game.

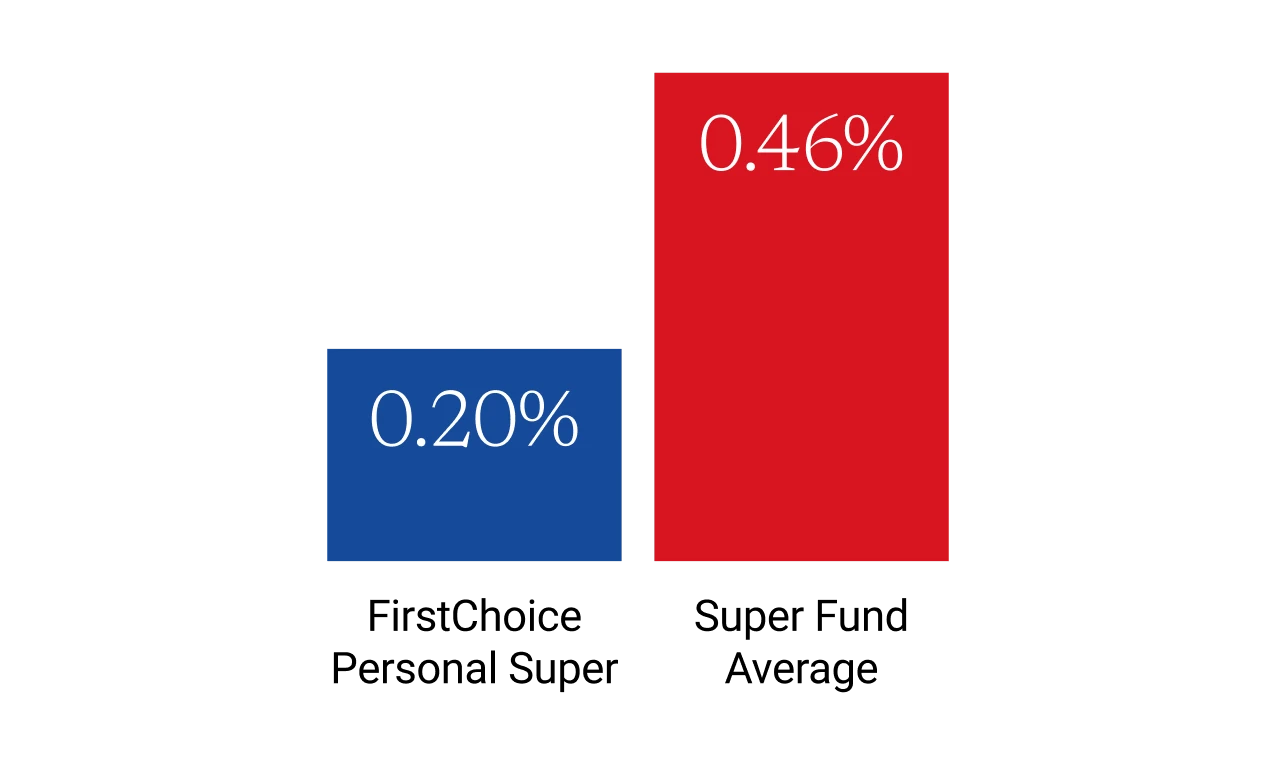

How CFS super fees compare

See how CFS FirstChoice Wholesale Personal Super and CFS FirstChoice Employer Super stacks up against the super fund average.

FirstChoice Wholesale Personal Super has one of the lowest admin fees in the market²

Source: Chant West Super Fund Fee Survey, March 2026.

This chart shows the administration fees for FirstChoice Wholesale Personal Super options (excluding FirstRate options) on a $50,000 balance being 0.20% compared to the Super Fund Average of 0.46%. This does not include investment fees, costs, or transaction costs. Super Fund Average administration fees are based on the Chant West Super Fund Fee Survey, which compares average fees by segment and across five investment risk categories.

FirstChoice Employer Super has lower fees than the super funds average³

Source: Chant West Super Fund Fee Survey, March 2026.

This chart shows the annual fee of the CFS Lifestage 1965–69 option with a $50,000 balance in FirstChoice Employer Super is $395, compared to the All Funds Average of $445, and the Industry Funds Average of $450. Fees for FirstChoice Employer Super, the All Funds Average and the Industry Funds Average are compared for MySuper products based on data from the Chant West Super Fund Fee Survey. Fees may vary for other age cohorts, typically ranging between $375 and $400.

All fees and costs are detailed in our Product Disclosure Statement (PDS). Before you join, make sure to read the PDS and Target Market Determination (TMD) to help you decide if the product is right for you.

What fees do super funds charge?

Understanding super fees helps you make a smarter comparison. Here are the main types of fees you'll see across most super funds.

Administration fees

Admin fees cover the cost of running your super account which includes record-keeping, compliance, member services, and ongoing account management. These fees are typically charged as a percentage of your balance (% p.a.) or a flat dollar amount, or a combination of both.

Investment fees and costs

Investment fees cover the cost of managing the investment options your super is invested in, and these vary depending on the options you choose. Generally, a simple index fund will have lower investment fees than an actively managed option. CFS offers over 200 investment options, so you can review the fees and costs for each option in the Product Disclosure Statement (PDS).

Transaction costs

Transaction costs occur when a fund buys and sells investments. These can include brokerage fees, government taxes or charges, bank and custodian fees, and the buy/sell spreads from underlying investments.

For most options, there is a difference between the unit price used to issue and redeem units and the value of the option’s assets. This difference is due to what is called the buy/sell spread. If it costs more to buy an investment than you would receive from selling it at that time, the difference is also a transaction cost.

Transaction costs are usually small and are built into the unit price of your investment, rather than charged separately.

Other fees to watch for

Super funds may charge additional fees for extra services or support, or a greater choice of products.

CFS does not charge exit fees (now banned for most funds), and you can switch between investment options without incurring a switching fee.

If you have insurance cover through your super, the insurance premiums will be deducted from your account balance. A number of factors will determine how much you pay, including how much cover you have, your occupation and your health.

If you have an adviser, adviser service fees cover the cost of personal advice you receive from your financial adviser about your super.

Although each fee may appear to be small by itself, you need to think about how these will add up over the long term. These will be outlined in the Product Disclosure Statement (PDS).

What you get with CFS low fee super

Low fees doesn’t mean low value. With CFS, you get a competitive fee structure and a full-featured super fund.

Over 200 investment options

Choose from one of Australia's widest ranges of super investment options across key assets classes. Or let our CFS Lifestage option automatically manage your investment mix based on your age.

Investment performance

Small differences in both performance and fees can have a significant impact on your long-term returns. It’s worth considering whether benefits such as stronger investment performance justifies higher fees.

Access the CFS app

Easily manager your super in the CFS app. See your super working in real time with charts, insights, transaction history, and more. Track your performance, view your statements, and review your fees anytime.

Award-winning products and service

CFS has been independently recognised for delivering strong performance, low fees and exceptional service.

Ready to keep more of your super?

Join over three million Australians who've chosen CFS for low fees, strong performance, and real investment choice.

- Join CFS super online - it takes under 10 minutes

- Consolidate your super - we’ll help you bring your balance across from your previous fund

- Notify your employer - easily share your account information with your employer in our mobile app

Low Fee Super FAQs

There’s no single “cheapest” super fund. The total fees you pay depend on factors like your balance, chosen investment options, and the types of fees charged. When comparing super funds, it’s important to look at total fees, including administration, investment, and transaction costs, rather than focusing on one fee in isolation. The right super fund for you will depend on your personal circumstances and retirement goals, but choosing a fund with a combination of low fees and strong investment performance is a good place to start.

Details of the fees and other costs you may be charged are set out in the relevant Product Disclosure Statement (PDS). These costs may be deducted from your balance, from your investment returns, or from the assets of the super fund as a whole.

Additional fees, such as activity fees, personal advice fees, and insurance premiums, may also apply depending on the services or cover you choose. Entry and exit fees do not apply. Information about taxes, insurance fees, and other insurance‑related costs is provided in a separate section of the PDS.

It’s important to read all information relating to fees and costs, as they can affect your investment. Investment fees vary depending on the option you select and are detailed in the investment options tables in the PDS.

Lower fees mean more of your money stays invested, giving it greater potential to grow through the power of compounding. However, fees are only one part of the picture. Investment performance, available options, insurance, and service quality are also important considerations. The strongest outcomes come from a fund that balances competitive fees with strong long‑term returns, which is what CFS aims to deliver.

To compare super fund fees fairly, focus on the total annual cost rather than just the administration fee. This includes admin fees, investment fees, and any additional costs outlined in the fund’s Product Disclosure Statement. Independent rating agencies like Chant West, SuperRatings, and Canstar publish fee comparisons at a fund level. You can also use our funds and performance tool to see how our investment options compare.

Yes, switching super funds in Australia is straightforward. You can join CFS super online in under 10 minutes, and we can help you consolidate super from your previous fund into your new CFS account. Before making the switch, check whether you'll lose any insurance cover attached to your current fund, and consider any exit or withdrawal fees that might apply.

We're here to help

Get in touch

Get in touch with us online or call us 8:30am to 6pm (Sydney time) Monday to Friday.

Find the right advice option

Our dedicated team can help you choose from a range of different financial advice options.

Download mobile app

Track your balance and see your transaction history from anywhere.

¹ Administration fees of FirstChoice Wholesale Personal Super options (excluding FirstRate options) for a member balance of $50,000, is 0.20% p.a. effective December 2025. It does not take into consideration investment fees and costs or transaction costs. Please see the PDS for these fees and costs. Super fund Average admin fees are based on the Chant West Super Fund Fee Survey at 31 December 2025 that compares average fees by segments and across four investment risk categories.

² Administration fees for FirstChoice Wholesale Personal Super options (excluding FirstRate options) are for a member balance of $50,000. It does not take into consideration investment fees and costs or transaction costs. Please see the PDS for these fees and costs.

Super Fund Average admin fees are based on the Chant West Super Fund Fee Survey that compares average fees by segments and across five investment risk categories.

The chart is constructed by CFS using data sourced from the Chant West Super Fund Fee Survey, which is based on information provided to Chant West by third parties that is believed accurate at the time of publication. Fees may change in the future which may affect the outcome of the comparison. Chant West may make adjustments to fees and costs for comparison purposes and therefore data may vary to other published materials. Consider the PDS and TMD to see if it’s right for you.

³ The fee comparison applies to MySuper products and is based on the CFS Lifestage 1965-69 option for a member balance of $50,000. Fees may vary for different age cohorts. The Chant West Super Fund Fee Survey compares the CFS Lifestage option that is closest to 71% growth assets, which is consistent with the average risk and return profile of most non-lifecycle products. Total fees and costs include administration fees and costs, investment fees and costs, and net transaction costs, calculated on a gross of tax basis. Fund averages are calculated by Chant West on a weighted average basis. This comparison has been prepared by CFS using data sourced from the Chant West Super Fund Fee Survey and is based on information provided to Chant West by third parties, that is believed accurate at the time of publication. Fees may change in the future which may affect the outcome of the comparison. Chant West may make adjustments to fees and costs for comparison purposes and therefore data may vary to other published materials. Whilst care has been taken to ensure that the data provided by Chant West is correct, CFS neither warrants, represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein.

Disclaimer

Avanteos Investments Limited ABN 20 096 259 979, AFSL 245531 (AIL) is the trustee of the Colonial First State FirstChoice Superannuation Trust ABN 26 458 298 557 and issuer of FirstChoice range of super and pension products. Colonial First State Investments Limited ABN 98 002 348 352, AFSL 232468 (CFSIL) is the responsible entity and issuer of products made available under FirstChoice Investments and FirstChoice Wholesale Investments.

Information on this webpage is provided by AIL and CFSIL. It may include general advice but does not consider your individual objectives, financial situation, needs or tax circumstances. You can find the target market determinations (TMD) for our financial products at https://www.cfs.com.au/tmd which include a description of who a financial product might suit. You should read the relevant Product Disclosure Statement (PDS) and Financial Services Guide (FSG) carefully, assess whether the information is appropriate for you, and consider talking to a financial adviser before making an investment decision. You can get the PDS and FSG at www.cfs.com.au or by calling us on 13 13 36.